from google.colab import data_table

data_table.enable_dataframe_formatter() # Enabling an interactive DataFrame displayLasso Linear Regression

Online Shopping

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.preprocessing import scale # zero mean & one s.d.

from sklearn.linear_model import LassoCV, lasso_path

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_squared_error

df = pd.read_csv("https://bcdanl.github.io/data/browser-online-shopping.zip")

dfWarning: Total number of columns (1001) exceeds max_columns (20). Falling back to pandas display.| spend | atdmt.com | yahoo.com | whenu.com | weatherbug.com | msn.com | google.com | aol.com | questionmarket.com | googlesyndication.com-o02 | ... | ugo.com | cox.com | spicymint.com | real.com-o01 | targetnet.com | effectivebrand.com | dallascowboys.com | leadgenetwork.com | in.us | vistaprint.com | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 424 | 4.052026 | 11.855928 | 0.000000 | 0.000000 | 0.250125 | 6.528264 | 0.150075 | 1.350675 | 3.401701 | ... | 0.0 | 0.025013 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.000000 |

| 1 | 2335 | 4.448743 | 8.446164 | 0.000000 | 0.000000 | 0.644745 | 0.451322 | 0.128949 | 0.967118 | 1.225016 | ... | 0.0 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.000000 |

| 2 | 279 | 7.678815 | 0.487234 | 0.000000 | 31.904112 | 13.213798 | 0.954980 | 0.000000 | 2.124342 | 2.514130 | ... | 0.0 | 0.000000 | 0.000000 | 0.019489 | 0.019489 | 0.0 | 0.0 | 0.0 | 0.0 | 0.000000 |

| 3 | 829 | 13.547802 | 18.509289 | 0.045310 | 0.045310 | 0.294517 | 1.110104 | 0.067966 | 3.194382 | 3.149071 | ... | 0.0 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.067966 |

| 4 | 221 | 2.879581 | 10.558464 | 0.000000 | 0.000000 | 3.606748 | 1.396161 | 0.000000 | 0.727167 | 0.988947 | ... | 0.0 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.000000 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 9995 | 102 | 6.040454 | 26.350790 | 0.000000 | 0.000000 | 0.000000 | 0.055417 | 4.710446 | 2.909393 | 0.554170 | ... | 0.0 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.000000 |

| 9996 | 5096 | 8.044292 | 3.012539 | 9.102752 | 0.032568 | 1.612115 | 1.840091 | 9.037616 | 3.289367 | 1.009608 | ... | 0.0 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.000000 |

| 9997 | 883 | 7.053942 | 1.659751 | 0.000000 | 0.000000 | 9.543568 | 0.414938 | 13.692946 | 2.074689 | 2.074689 | ... | 0.0 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.000000 |

| 9998 | 256 | 10.408043 | 0.473093 | 0.000000 | 0.000000 | 18.568894 | 0.887049 | 3.370787 | 3.548196 | 0.236546 | ... | 0.0 | 0.532229 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.000000 |

| 9999 | 6 | 2.937832 | 11.789234 | 0.018954 | 7.827900 | 0.113723 | 2.710387 | 0.151630 | 0.777104 | 0.398029 | ... | 0.0 | 0.000000 | 0.037908 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.000000 |

10000 rows × 1001 columns

X = df.drop('spend', axis = 1)

y = df['spend']

# Train-test split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)

X_train_np = X_train.values

X_test_np = X_test.values

y_train_np = y_train.values

y_test_np = y_test.values# LassoCV with a range of alpha values

lasso_cv = LassoCV(n_alphas = 100, # default is 100

alphas = None, # alphas=None automatically generate 100 candidate alpha values

cv = 5,

random_state=42,

max_iter=100000)

lasso_cv.fit(X_train.values, np.log(y_train.values))

print("LassoCV - Best alpha:", lasso_cv.alpha_)

# Create a DataFrame including the intercept and the coefficients:

coef_lasso = pd.DataFrame({

'predictor': list(X_train.columns),

'coefficient': list(lasso_cv.coef_),

'exp_coefficient': np.exp( list(lasso_cv.coef_) )

})

# Evaluate

y_pred_lasso = lasso_cv.predict(X_test.values)

mse_lasso = mean_squared_error(y_test, y_pred_lasso)

print("LassoCV - MSE:", mse_lasso)LassoCV - Best alpha: 0.004098154620620373

LassoCV - MSE: 88099012.81854005# LassoCV with a range of alpha values

lasso_cv = LassoCV(n_alphas = 100, # default is 100

alphas = None, # alphas=None automatically generate 100 candidate alpha values

cv = 5,

random_state=42,

max_iter=100000)

lasso_cv.fit(X_train_np, np.log(y_train_np))

print("LassoCV - Best alpha:", lasso_cv.alpha_)

# Create a DataFrame including the intercept and the coefficients:

coef_lasso = pd.DataFrame({

'predictor': list(X_train.columns),

'coefficient': list(lasso_cv.coef_),

'exp_coefficient': np.exp( list(lasso_cv.coef_) )

})

# Evaluate

y_pred_lasso = lasso_cv.predict(X_test_np)

mse_lasso = mean_squared_error(y_test_np, y_pred_lasso)

print("LassoCV - MSE:", mse_lasso)LassoCV - Best alpha: 0.004098154620620373

LassoCV - MSE: 88099012.81854005coef_lasso = coef_lasso.query('coefficient != 0')

coef_lasso.shape[0]307coef_lasso.sort_values('coefficient', ascending = False)| predictor | coefficient | exp_coefficient | |

|---|---|---|---|

| 895 | bizrate.com-o01 | 1.388699 | 4.009628 |

| 770 | staples.com | 0.757120 | 2.132127 |

| 690 | travelhook.net | 0.688146 | 1.990022 |

| 843 | united.com | 0.610771 | 1.841850 |

| 506 | victoriassecret.com | 0.584030 | 1.793251 |

| ... | ... | ... | ... |

| 279 | new.net | -0.181475 | 0.834039 |

| 374 | coolsavings.com | -0.187875 | 0.828718 |

| 851 | rsc03.net | -0.231599 | 0.793264 |

| 443 | checkm8.com | -0.240327 | 0.786371 |

| 481 | macromedia.com | -0.243739 | 0.783693 |

307 rows × 3 columns

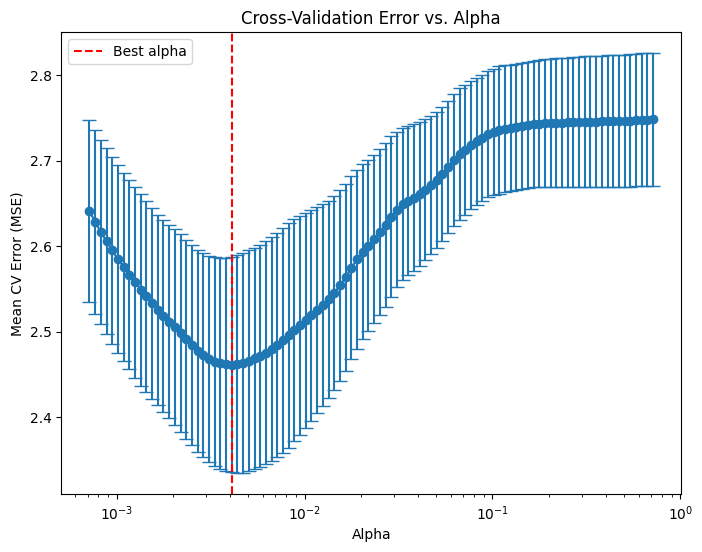

# Compute the mean and standard deviation of the CV errors for each alpha.

mean_cv_errors = np.mean(lasso_cv.mse_path_, axis=1)

std_cv_errors = np.std(lasso_cv.mse_path_, axis=1)

plt.figure(figsize=(8, 6))

plt.errorbar(lasso_cv.alphas_, mean_cv_errors, yerr=std_cv_errors, marker='o', linestyle='-', capsize=5)

plt.xscale('log')

plt.xlabel('Alpha')

plt.ylabel('Mean CV Error (MSE)')

plt.title('Cross-Validation Error vs. Alpha')

#plt.gca().invert_xaxis() # Optionally invert the x-axis so lower alphas (less regularization) appear to the right.

plt.axvline(x=lasso_cv.alpha_, color='red', linestyle='--', label='Best alpha')

plt.legend()

plt.show()

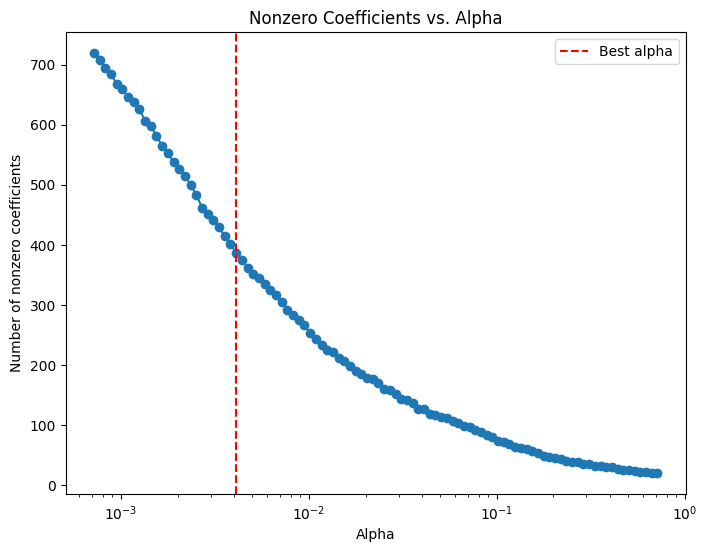

# Compute the coefficient path over the alpha grid that LassoCV used

alphas, coefs, _ = lasso_path(X_train, np.log(y_train),

alphas=lasso_cv.alphas_,

max_iter=100000)

# Count nonzero coefficients for each alpha (coefs shape: (n_features, n_alphas))

nonzero_counts = np.sum(coefs != 0, axis=0)

# Plot the number of nonzero coefficients versus alpha

plt.figure(figsize=(8,6))

plt.plot(alphas, nonzero_counts, marker='o', linestyle='-')

plt.xscale('log')

plt.xlabel('Alpha')

plt.ylabel('Number of nonzero coefficients')

plt.title('Nonzero Coefficients vs. Alpha')

#plt.gca().invert_xaxis() # Lower alphas (less regularization) on the right

plt.axvline(x=lasso_cv.alpha_, color='red', linestyle='--', label='Best alpha')

plt.legend()

plt.show()

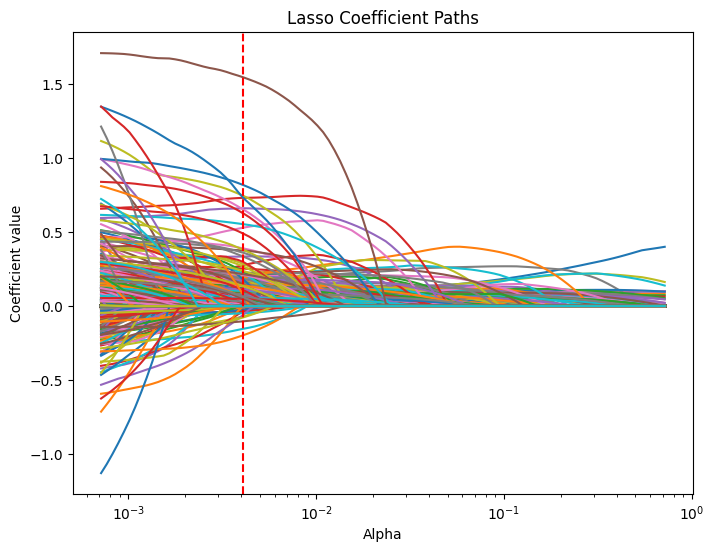

# Compute the lasso path. Note: we use np.log(y_train) because that's what you used in LassoCV.

alphas, coefs, _ = lasso_path(X_train.values, np.log(y_train.values), alphas=lasso_cv.alphas_, max_iter=100000)

plt.figure(figsize=(8, 6))

# Iterate over each predictor and plot its coefficient path.

for i, col in enumerate(X_train.columns):

plt.plot(alphas, coefs[i, :], label=col)

plt.xscale('log')

plt.xlabel('Alpha')

plt.ylabel('Coefficient value')

plt.title('Lasso Coefficient Paths')

#plt.gca().invert_xaxis() # Lower alphas (weaker regularization) to the right.

#plt.legend(bbox_to_anchor=(1.05, 1), loc='upper left')

plt.axvline(x=lasso_cv.alpha_, color='red', linestyle='--', label='Best alpha')

#plt.legend()

plt.show()

# RidgeCV with a list of alpha values and 3-fold cross-validation

from sklearn.linear_model import RidgeCV, Ridge

alpha_max = 10

alpha_min_ratio = 1e-4

alpha_min = alpha_max * alpha_min_ratio

# Define candidate alpha values

alphas = np.logspace(np.log(alpha_max), np.log(alpha_min), num=5)

alphasarray([2.00717432e+02, 1.00000000e+00, 4.98212830e-03, 2.48216024e-05,

1.23664407e-07])

ridge_cv = RidgeCV(alphas=alphas, cv=3, scoring='neg_mean_squared_error')

ridge_cv.fit(X_train_np, np.log(y_train_np))

print("RidgeCV - Best alpha:", ridge_cv.alpha_)

# Create a DataFrame including the intercept and the coefficients:

coef_ridge = pd.DataFrame({

'predictor': list(X_train.columns),

'coefficient': list(ridge_cv.coef_),

'exp_coefficient': np.exp( list(ridge_cv.coef_) )

})

# Evaluate

y_pred_ridge = ridge_cv.predict(X_test_np)

mse_ridge = mean_squared_error(y_test_np, y_pred_ridge)

print("RidgeCV - MSE:", mse_ridge)

RidgeCV - Best alpha: 200.71743249053017

RidgeCV - MSE: 88099136.93994579coef_ridge| predictor | coefficient | exp_coefficient | |

|---|---|---|---|

| 0 | atdmt.com | -0.004977 | 0.995035 |

| 1 | yahoo.com | -0.017194 | 0.982953 |

| 2 | whenu.com | -0.008336 | 0.991699 |

| 3 | weatherbug.com | -0.005399 | 0.994616 |

| 4 | msn.com | -0.004900 | 0.995112 |

| ... | ... | ... | ... |

| 995 | effectivebrand.com | -0.098469 | 0.906223 |

| 996 | dallascowboys.com | -0.039989 | 0.960800 |

| 997 | leadgenetwork.com | 0.009274 | 1.009317 |

| 998 | in.us | -0.033527 | 0.967029 |

| 999 | vistaprint.com | 0.066156 | 1.068394 |

1000 rows × 3 columns

coef_ridge.query('coefficient != 0').shape[0]1000ridge = Ridge()

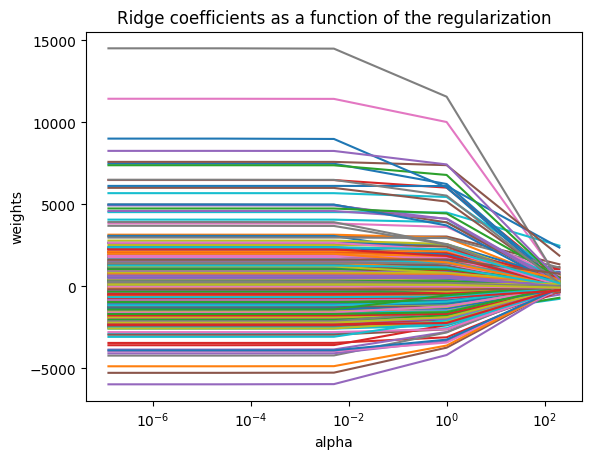

coefs = []

for a in alphas:

ridge.set_params(alpha=a)

ridge.fit(X_train_np, y_train_np)

coefs.append(ridge.coef_)

ax = plt.gca()

ax.plot(alphas, coefs)

ax.set_xscale('log')

#ax.set_xlim(ax.get_xlim()[::-1]) # reverse axis

plt.axis('tight')

plt.xlabel('alpha')

plt.ylabel('weights')

plt.title('Ridge coefficients as a function of the regularization');