library(tidyverse)

library(janitor)

library(ggthemes)

library(rmarkdown)

library(rpart)

library(rpart.plot)

library(ranger)

library(vip)

library(pdp)

# library(xgboost) # load this right before we use xgboost()Random Forest and Gradient-Boosted Trees

Boston Housing Data

Boston Housing Data

boston <- read_csv("https://bcdanl.github.io/data/boston.csv") |>

janitor::clean_names()

paged_table(boston)Modeling goal

- Predict

medv, median housing value in thousands of dollars - Boston housing is a classic regression example with multiple socioeconomic and neighborhood predictors

- We will use it to study overfitting, pruning, random forests, and boosting

Create training and test data

set.seed(42120532)

boston <- boston |>

mutate(rnd = runif(n()))

dtrain <- boston |>

filter(rnd > .2) |>

select(-rnd)

dtest <- boston |>

filter(rnd <= .2) |>

select(-rnd)

x_train <- dtrain |> select(-medv)

y_train <- dtrain$medv

x_test <- dtest |> select(-medv)

y_test <- dtest$medvRandom Forest

Fit an initial random forest on Boston housing

set.seed(1917)

init_boston_rf <- ranger(

medv ~ .,

data = dtrain,

num.trees = 300,

importance = "permutation"

)

init_boston_rfRanger result

Call:

ranger(medv ~ ., data = dtrain, num.trees = 300, importance = "permutation")

Type: Regression

Number of trees: 300

Sample size: 392

Number of independent variables: 13

Mtry: 3

Target node size: 5

Variable importance mode: permutation

Splitrule: variance

OOB prediction error (MSE): 11.83664

R squared (OOB): 0.8582419 Important ranger() arguments

init_boston_rf$num.trees[1] 300init_boston_rf$mtry[1] 3init_boston_rf$prediction.error[1] 11.83664init_boston_rf$min.node.size[1] 5init_boston_rf$importance[1] "permutation"num.trees: number of trees in the forestmtry: number of predictors considered at each splitprediction.error: out-of-bag error estimate.min.node.size: minimum terminal node sizeimportance: method used to calculate variable importance"none": do not compute variable importance (default)"impurity": compute importance based on total impurity reduction from splits"permutation": compute importance based on how much model performance worsens when a variable is shuffled

Interpreting the ranger output

Tune mtry

No loop

rf_2 <- ranger(

medv ~ .,

data = dtrain,

num.trees = 300,

mtry = 2,

importance = "permutation"

)

rf_4 <- ranger(

medv ~ .,

data = dtrain,

num.trees = 300,

mtry = 4,

importance = "permutation"

)

rf_6 <- ranger(

medv ~ .,

data = dtrain,

num.trees = 300,

mtry = 6,

importance = "permutation"

)

rf_8 <- ranger(

medv ~ .,

data = dtrain,

num.trees = 300,

mtry = 8,

importance = "permutation"

)

rf_10 <- ranger(

medv ~ .,

data = dtrain,

num.trees = 300,

mtry = 10,

importance = "permutation"

)

rf_12 <- ranger(

medv ~ .,

data = dtrain,

num.trees = 300,

mtry = 12,

importance = "permutation"

)

rf_results <- tibble(

mtry = c(2, 4, 6, 8, 10, 12),

oob_error = c(

rf_2$prediction.error,

rf_4$prediction.error,

rf_6$prediction.error,

rf_8$prediction.error,

rf_10$prediction.error,

rf_12$prediction.error

)

)

rf_results |>

paged_table()Loop

# p = the total number of predictor variables in the training data

p <- ncol(x_train)

# Create a tuning grid for mtry:

# mtry is the number of predictors randomly considered at each split

# Here, we try even-numbered values from 2 up to p

rf_grid <- tibble(mtry = seq(2, p, by = 2))

# Create an empty tibble to store the tuning results

# We will save each mtry value and its corresponding OOB error

rf_results <- tibble(

mtry = numeric(),

oob_error = numeric()

)

# Loop over each candidate mtry value

for (m in rf_grid$mtry) {

# Fit a random forest model with the current mtry value

fit <- ranger(

medv ~ .,

data = dtrain,

num.trees = 300, # grow 300 trees in the forest

mtry = m, # current candidate value of mtry

importance = "permutation" # compute permutation-based variable importance

)

# Store the current mtry value and its OOB prediction error

rf_results <- bind_rows(

rf_results,

tibble(

mtry = m,

oob_error = fit$prediction.error

)

)

}

rf_results |>

paged_table()Plot the tuning results

rf_results |>

ggplot(aes(x = mtry, y = oob_error)) +

geom_line() +

geom_point() +

labs(

title = "Random Forest Tuning Results",

x = "mtry",

y = "Out-of-bag prediction error"

)

Final random forest

best_mtry <- rf_results |>

slice_min(oob_error, n = 1) |>

pull(mtry)

final_boston_rf <- ranger(

medv ~ .,

data = dtrain,

num.trees = 500,

mtry = best_mtry,

importance = "permutation"

)

best_mtry[1] 10final_boston_rfRanger result

Call:

ranger(medv ~ ., data = dtrain, num.trees = 500, mtry = best_mtry, importance = "permutation")

Type: Regression

Number of trees: 500

Sample size: 392

Number of independent variables: 13

Mtry: 10

Target node size: 5

Variable importance mode: permutation

Splitrule: variance

OOB prediction error (MSE): 9.527965

R squared (OOB): 0.8858911 Test performance of the random forest

rf_test_pred <- predict(final_boston_rf, data = dtest)$predictions

sqrt(mean((y_test - rf_test_pred)^2))[1] 3.075023Random forest variable importance

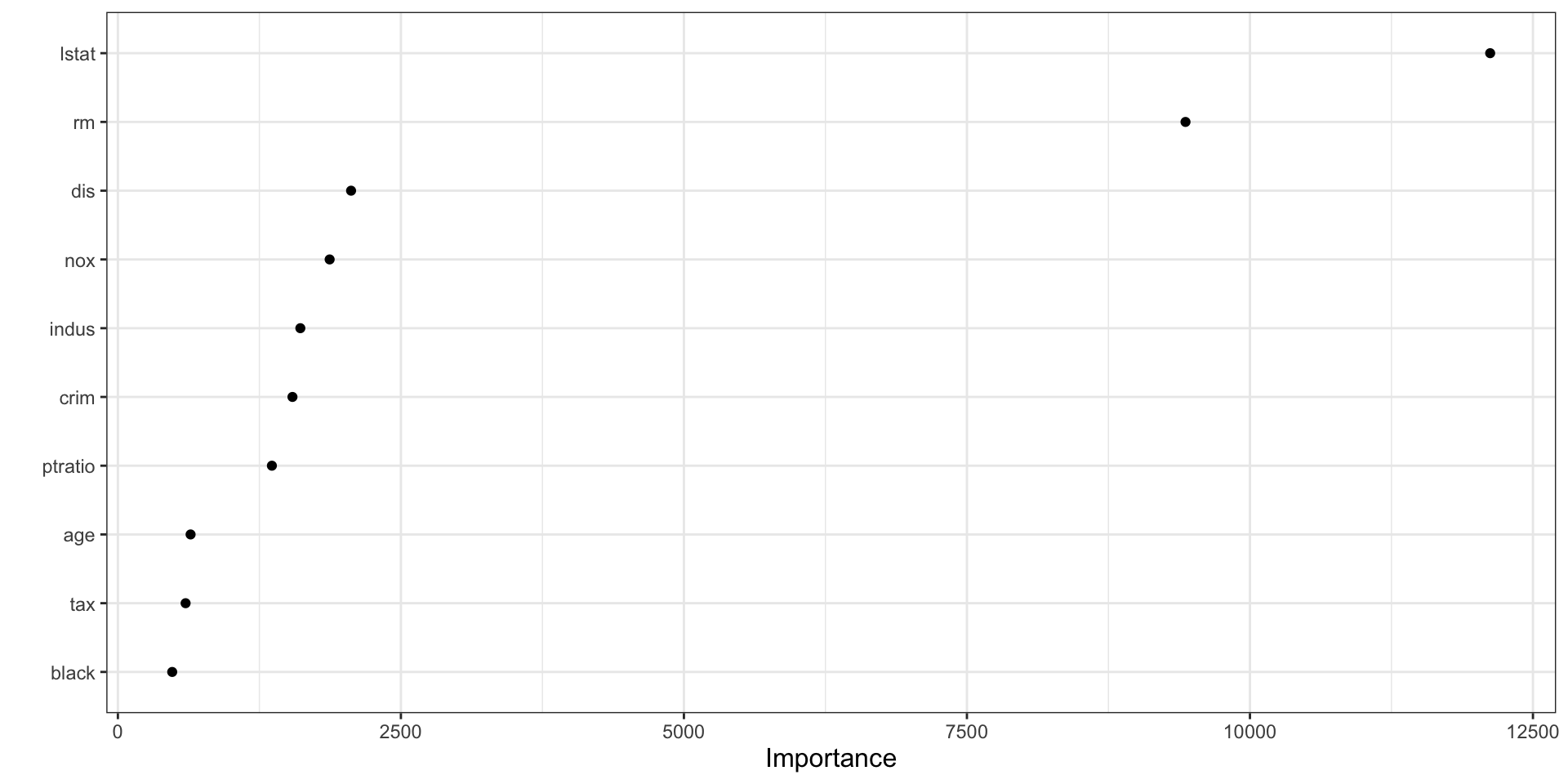

vip(final_boston_rf)

How to interpret vip() for a random forest

- The plot shows which predictors contributed most across the ensemble of trees.

- Higher importance means a variable was more useful in improving splits across the forest.

- In forests, importance is often more stable than in a single tree because it aggregates over many trees.

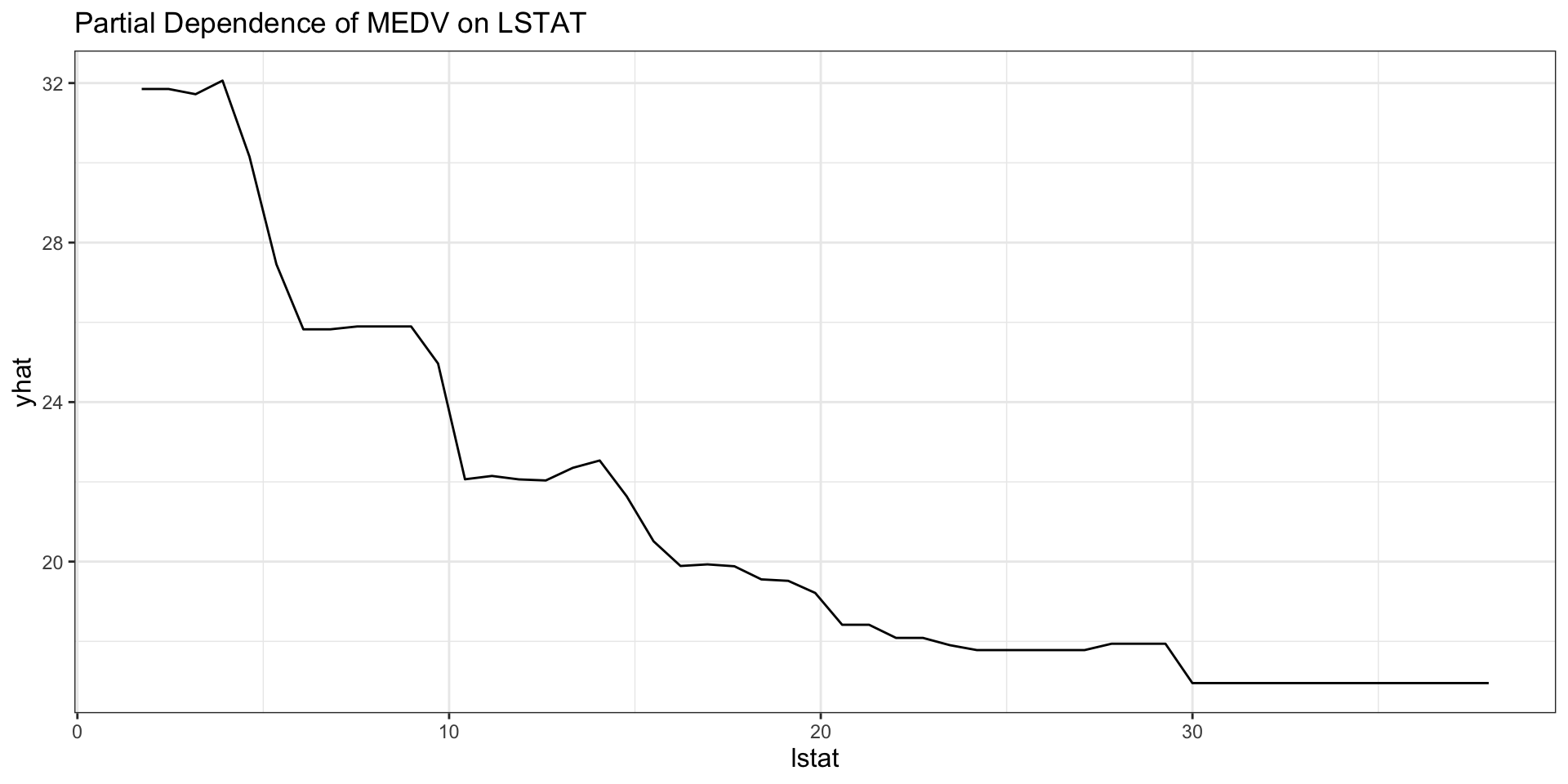

Partial dependence from the forest

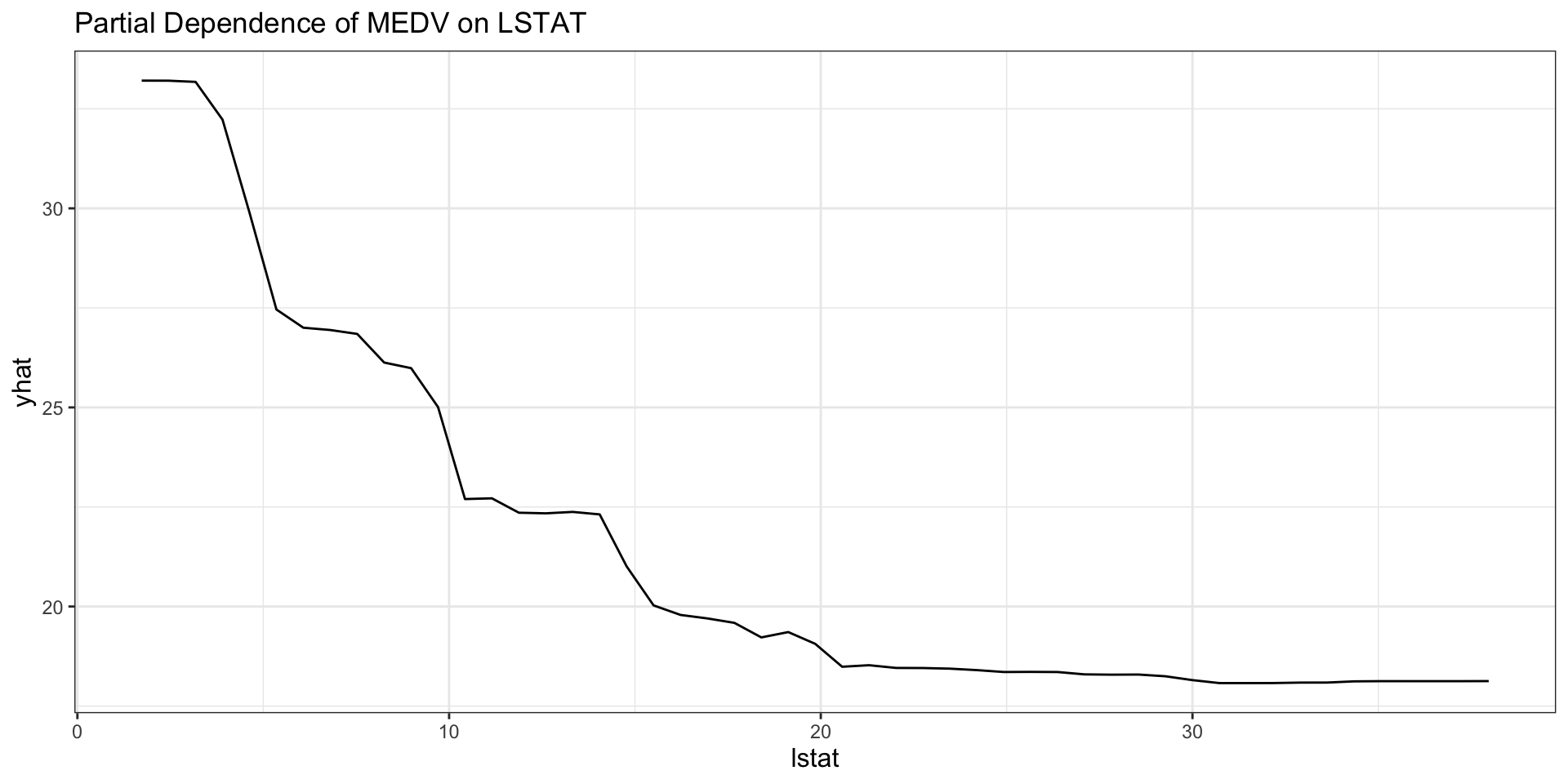

partial(final_boston_rf, pred.var = "lstat", train = x_train) |>

autoplot() +

labs(title = "Partial Dependence of MEDV on LSTAT")

Interpreting the random-forest PDP

- The curve shows the model’s average predicted

medvaslstatchanges. - All other variables are averaged over their observed values.

- Nonlinearity in the curve suggests that the marginal relationship is not well described by a straight line.

- Flat regions suggest limited marginal predictive contribution in that range.

Gradient-Boosted Trees

Key XGBoost tuning arguments

nrounds: number of boosting iterationseta: learning ratemax_depth: depth of each treegamma: minimum improvement required for a splitsubsample: fraction of observations used for each boosting stepcolsample_bytree: fraction of predictors used for each treemin_child_weight: minimum total weight allowed in a child node

How to think about the main tuning parameters

- Smaller

etameans slower learning and usually requires largernrounds. - Larger

max_depthallows more complex interactions. - Larger

gammamakes splitting more conservative. - Smaller

subsampleandcolsample_bytreecan reduce overfitting by injecting randomness. nroundsandetausually need to be tuned together.

Prepare matrix input for XGBoost

x_train_mat <- as.matrix(x_train)

x_test_mat <- as.matrix(x_test)Fit an initial XGBoost model

library(xgboost)

set.seed(1937)

xgb_fit_initial <- xgboost(

data = x_train_mat,

label = y_train,

objective = "reg:squarederror",

nrounds = 100,

eta = 0.1,

max_depth = 3,

verbose = 0

)

xgb_fit_initialXGBoost model object

Call:

xgboost(objective = "reg:squarederror", nrounds = 100, max_depth = 3,

data = x_train_mat, label = y_train, eta = 0.1, verbose = 0)

Objective: reg:squarederror

Number of iterations: 100

Number of features: 13What does the initial model represent?

- It is a sum of many shallow trees, not one large tree.

- Each boosting round adds a small correction to the current prediction.

objective in xgboost()

objective = "reg:squarederror"is used for a regression problem, where the response variable is continuous.- It tells XGBoost to predict a numeric outcome and minimize squared prediction error.

objective = "binary:logistic"is used for a binary classification problem, where the response variable has two classes such as0and1.- It tells XGBoost to predict the probability that an observation belongs to class

1.

- It tells XGBoost to predict the probability that an observation belongs to class

Simple tuning grid

xgb_grid <- tidyr::crossing(

nrounds = seq(50, 250, by = 50),

eta = c(0.025, 0.05, 0.1),

max_depth = c(1, 2, 3, 4),

gamma = c(0, 1),

colsample_bytree = c(0.8, 1),

min_child_weight = 1,

subsample = c(0.8, 1)

)

xgb_grid |>

paged_table()tidyr::crossing() generates all possible combinations of the supplied values, which is exactly what you want for a manual grid search.

- Grid size: 5 × 3 × 4 × 2 × 2 × 1 × 2 = 480 combinations

min_child_weight = 1is held constant (scalar), while everything else is varied- Here,

nroundsandetaare treated independently — combinations likenrounds = 50, eta = 0.025(very slow learning, few rounds) will both be evaluated alongsidenrounds = 250, eta = 0.1- We can consider fixing

etaand using early stopping instead, which makesnroundsa ceiling rather than a tuning parameter

- We can consider fixing

Cross-validated tuning

xgb_results_lst <- vector("list", nrow(xgb_grid))

dMat_train <- xgb.DMatrix(data = x_train_mat, label = y_train)

for (i in seq_len(nrow(xgb_grid))) {

nrounds <- xgb_grid$nrounds[i]

eta <- xgb_grid$eta[i]

max_depth <- xgb_grid$max_depth[i]

gamma <- xgb_grid$gamma[i]

colsample_bytree <- xgb_grid$colsample_bytree[i]

min_child_weight <- xgb_grid$min_child_weight[i]

subsample <- xgb_grid$subsample[i]

cv_fit <- xgb.cv(

# data = x_train_mat,

# label = y_train,

# If an error occurs with the message including DMatrix, try:

data = dMat_train,

nrounds = nrounds,

nfold = 5,

objective = "reg:squarederror",

eta = eta,

max_depth = max_depth,

gamma = gamma,

colsample_bytree = colsample_bytree,

min_child_weight = min_child_weight,

subsample = subsample,

verbose = 0

)

xgb_results_lst[[i]] <- tibble(

nrounds = nrounds,

eta = eta,

max_depth = max_depth,

gamma = gamma,

colsample_bytree = colsample_bytree,

min_child_weight = min_child_weight,

subsample = subsample,

cv_rmse = min(cv_fit$evaluation_log$test_rmse_mean)

)

}

xgb_results <-

bind_rows(xgb_results_lst) |>

arrange(cv_rmse)

xgb_results |>

paged_table()Fit the final XGBoost model

# best_xgb <- xgb_results[order(xgb_results$cv_rmse), ][1, ]

best_xgb <- xgb_results |>

slice_min(cv_rmse, n = 1)

best_xgb |>

paged_table()xgb_fit_final <- xgboost(

data = x_train_mat,

label = y_train,

objective = "reg:squarederror",

nrounds = best_xgb$nrounds,

eta = best_xgb$eta,

max_depth = best_xgb$max_depth,

gamma = best_xgb$gamma,

colsample_bytree = best_xgb$colsample_bytree,

min_child_weight = best_xgb$min_child_weight,

subsample = best_xgb$subsample,

verbose = 0

)

xgb_fit_finalXGBoost model object

Call:

xgboost(objective = "reg:squarederror", nrounds = best_xgb$nrounds,

max_depth = best_xgb$max_depth, min_child_weight = best_xgb$min_child_weight,

subsample = best_xgb$subsample, colsample_bytree = best_xgb$colsample_bytree,

data = x_train_mat, label = y_train, eta = best_xgb$eta,

gamma = best_xgb$gamma, verbose = 0)

Objective: reg:squarederror

Number of iterations: 150

Number of features: 13Test performance of XGBoost

xgb_test_pred <- predict(xgb_fit_final, newdata = x_test_mat)

sqrt(mean((y_test - xgb_test_pred)^2))[1] 2.841075Variable Importance: A Free Byproduct of Ensembles

Both random forest and gradient boosting measure variable importance automatically

The key question: how much does each predictor contribute to reducing prediction error?

Random forest — permutation importance:

- For each variable, randomly shuffle its values and measure the drop in OOB accuracy

- A large drop → the variable was doing real work; a small drop → it barely mattered

Random forest — impurity importance:

- Tracks how much splits on a variable reduce impurity, summed across all trees

- In regression, impurity is usually based on reduction in outcome variance

- A larger total reduction means the variable was more useful for making cleaner splits

Gradient boosting — gain-based importance:

- Tracks how much each split on a variable reduced the loss function, summed across all trees

- Variables used in high-gain splits rank highly

Why This Matters

Unlike linear regression, tree ensembles can capture non-linear effects and interactions. Variable importance tells you which variables the model relies on most, even when the relationship between predictor and outcome is complex.

XGBoost variable importance

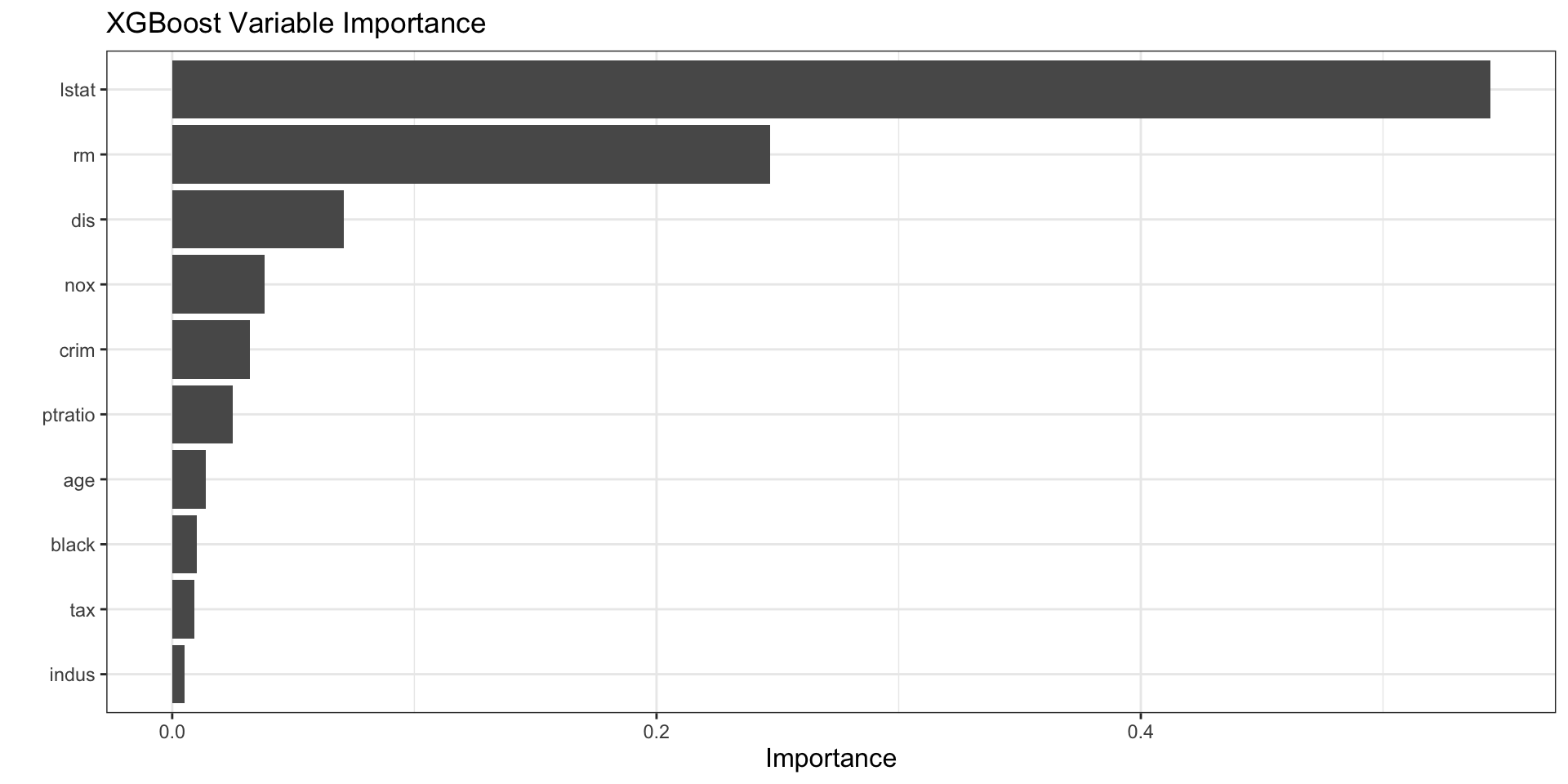

vip(xgb_fit_final) +

labs(title = "XGBoost Variable Importance")

How to interpret vip() for XGBoost

- XGBoost importance is based on how much each variable contributes across many boosting rounds.

- Variables near the top are most useful for reducing the loss function.

- Importance does not reveal the direction of the effect.

- A variable can be important because it appears in many small improvements, not only because it appears in one dominant split.

Partial dependence for XGBoost

partial(

xgb_fit_final,

pred.var = "lstat",

train = x_train_mat,

plot = TRUE,

plot.engine = "ggplot2",

type = "regression"

) +

labs(title = "Partial Dependence of MEDV on LSTAT")

Interpreting the XGBoost PDP

- The PDP summarizes the average fitted relationship between

lstatand predicted housing values. - Because XGBoost is highly flexible, the curve can show richer nonlinearities than a single tree.

- Sharp changes in the curve can indicate thresholds learned by the boosted ensemble.