Lecture 4

K-fold Cross-Validation; Bias-Variance Trade-off; Regularized Regression

February 25, 2026

K-fold Cross-Validation

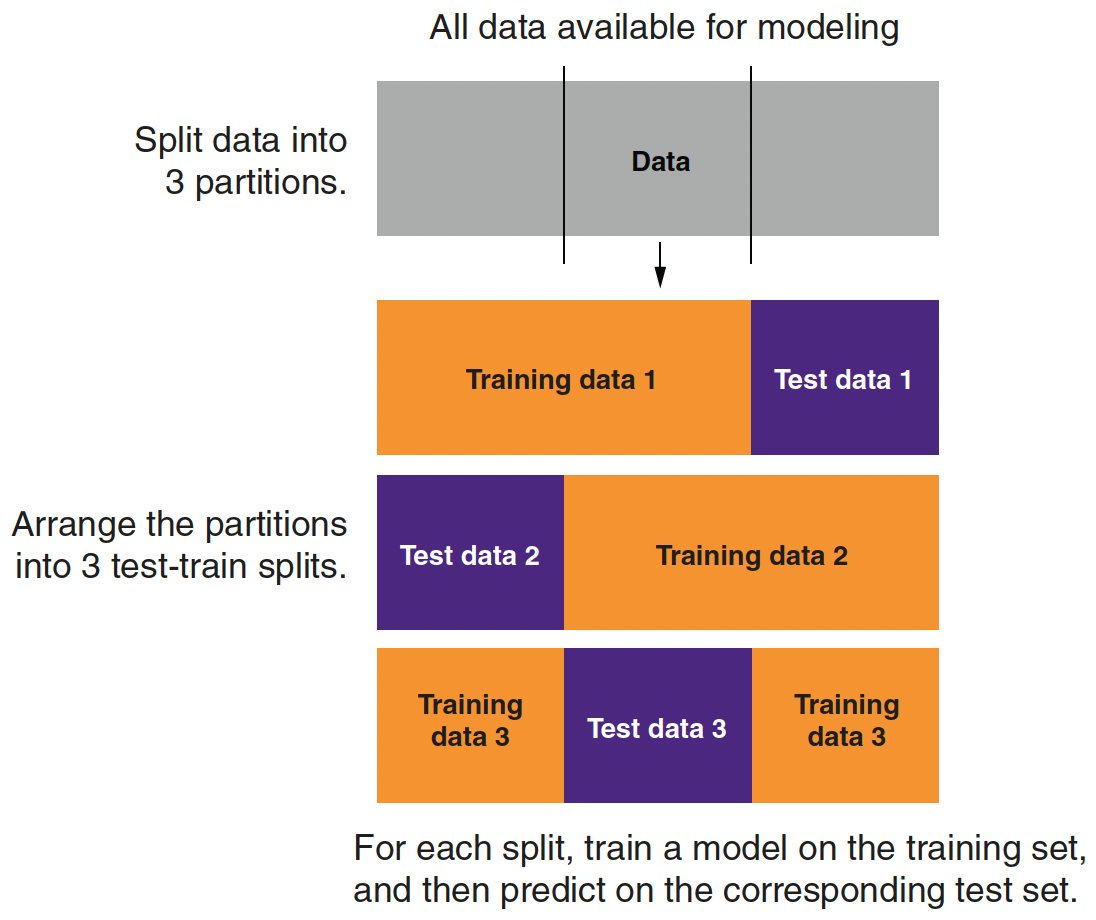

Partitioning Data for 3-fold Cross-Validation

Partitioning Data for 3-fold Cross-Validation

- A single train–test split uses each subset only once—either for training or for evaluation.

- K‑fold cross-validation divides the training data into K equal parts (folds).

- For each fold \(k=1, \dots, K\):

- Step 1: Train the model on \(K‑1\) folds.

- Step 2: Evaluate the model on the held‑out fold.

- For each fold \(k=1, \dots, K\):

- The average error across folds provides a robust estimate of model performance.

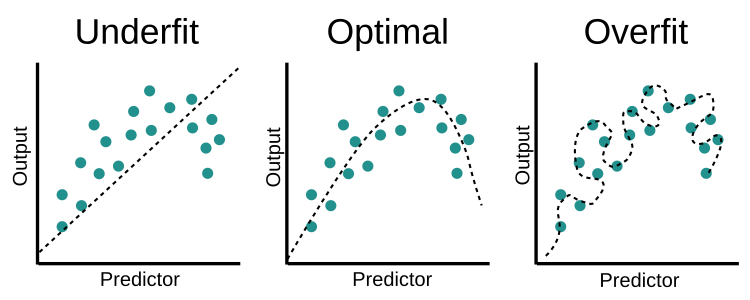

Underfit vs. Optimal vs. Overfit

- Underfit: too simple, so it misses the main structure (systematic pattern) in the data.

- Optimal: complex enough to capture the overall trend, but not so flexible that it chases noise.

- Overfit: fits the training points extremely well, but the curve is too sensitive to small changes, so the shape is not stable and generalizes poorly.

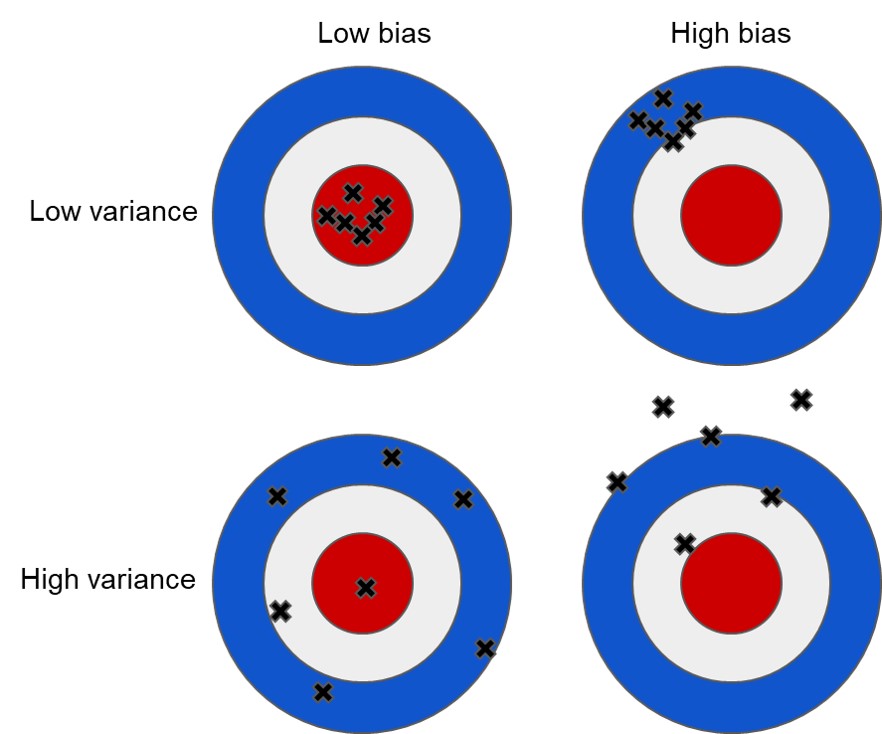

Bias vs. Variance

- Think of each black × as the model’s prediction from a different training sample.

- Low bias + low variance (top-left): accurate and stable → best generalization.

- High bias + low variance (top-right): stable but consistently wrong → underfitting.

- Low bias + high variance (bottom-left): right on average but noisy → overfitting risk.

- High bias + high variance (bottom-right): wrong and unstable → usually the worst case.

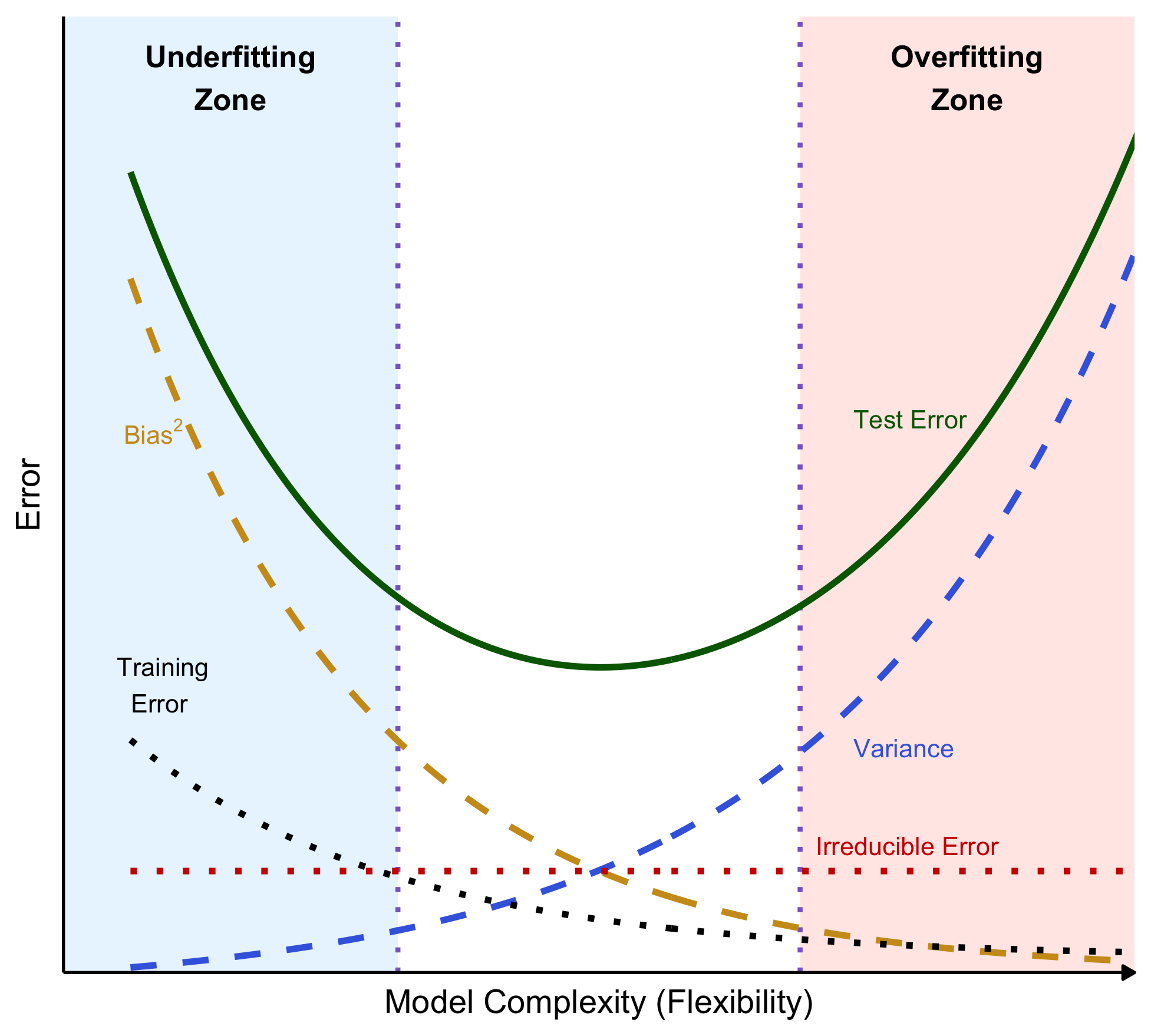

The Bias–Variance Trade-off Curve

- Bias\(^2\): simple models cannot represent complex patterns → high systematic error

- Adding flexibility lets the model capture real structure → lower bias

- Variance: flexible models adapt strongly to the specific training sample you happened to observe

- if you re-sample the training data, the fitted model can change a lot

- The “best” complexity is near the bottom of the U (minimum test error).

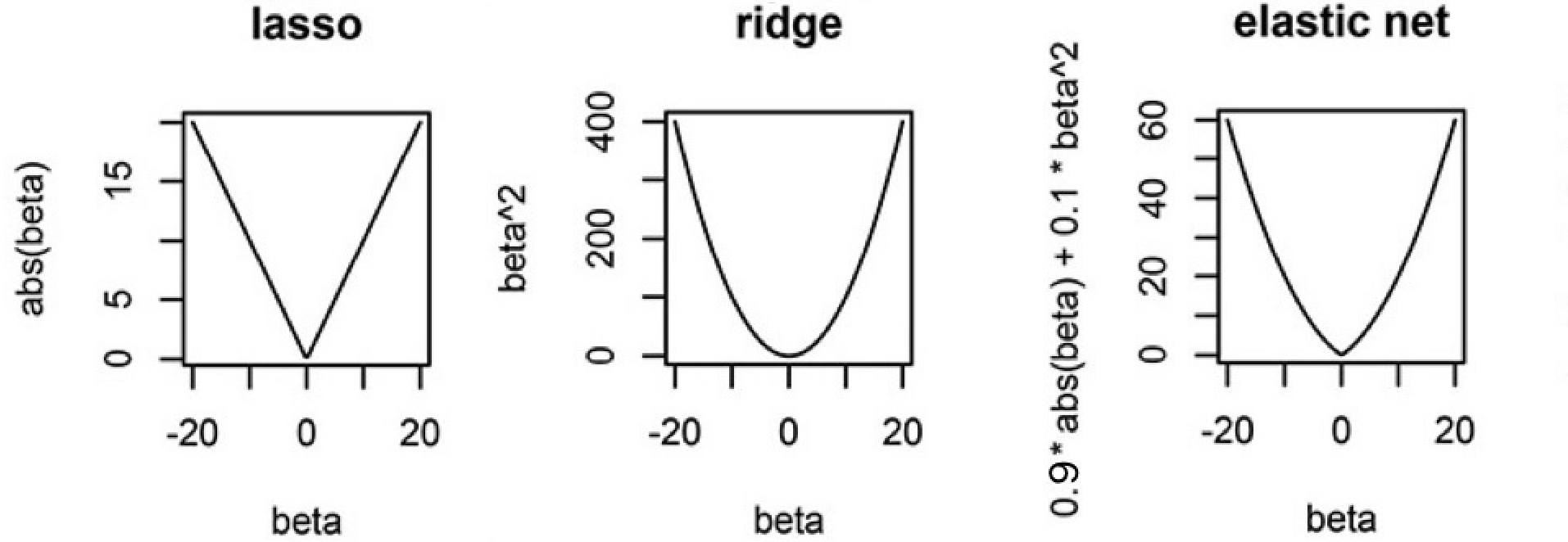

How Expensive Is It To Make \(\beta\) Large?

- Lasso (L1) Penalty (\(|\beta|\)):

- Each unit increase in \(\beta\) adds a constant penalty, regardless of \(\beta\) ’s size.

- Drives some coefficients exactly to zero, acting as a predictor selection mechanism.

- Ridge (L2) Penalty (\(\beta^2\)):

- Gently penalizes small-to-moderate deviations from zero, but penalty increases quickly for large \(\beta\).

- Shrinks coefficients but does not set them exactly to zero.

Intuition on Different Penalties

- The ellipses are contours of equal SSE (same fit quality).

- The shape is the constraint/penalty region.

- Lasso induces corner solutions!

- Lasso has corners, and corners create zeros.

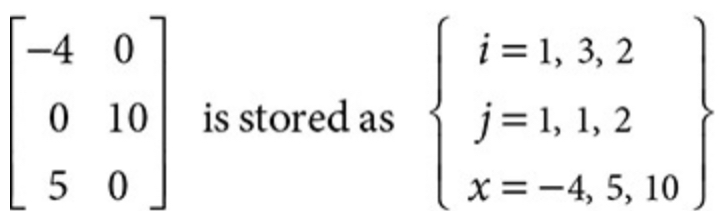

Sparse Matrix

R’s \(\texttt{glmnet}\) package uses a sparse matrix

A sparse matrix is a matrix with many zero entries

A sparse matrix is almost essential in big data analysis because of its lower storage costs and faster computation.

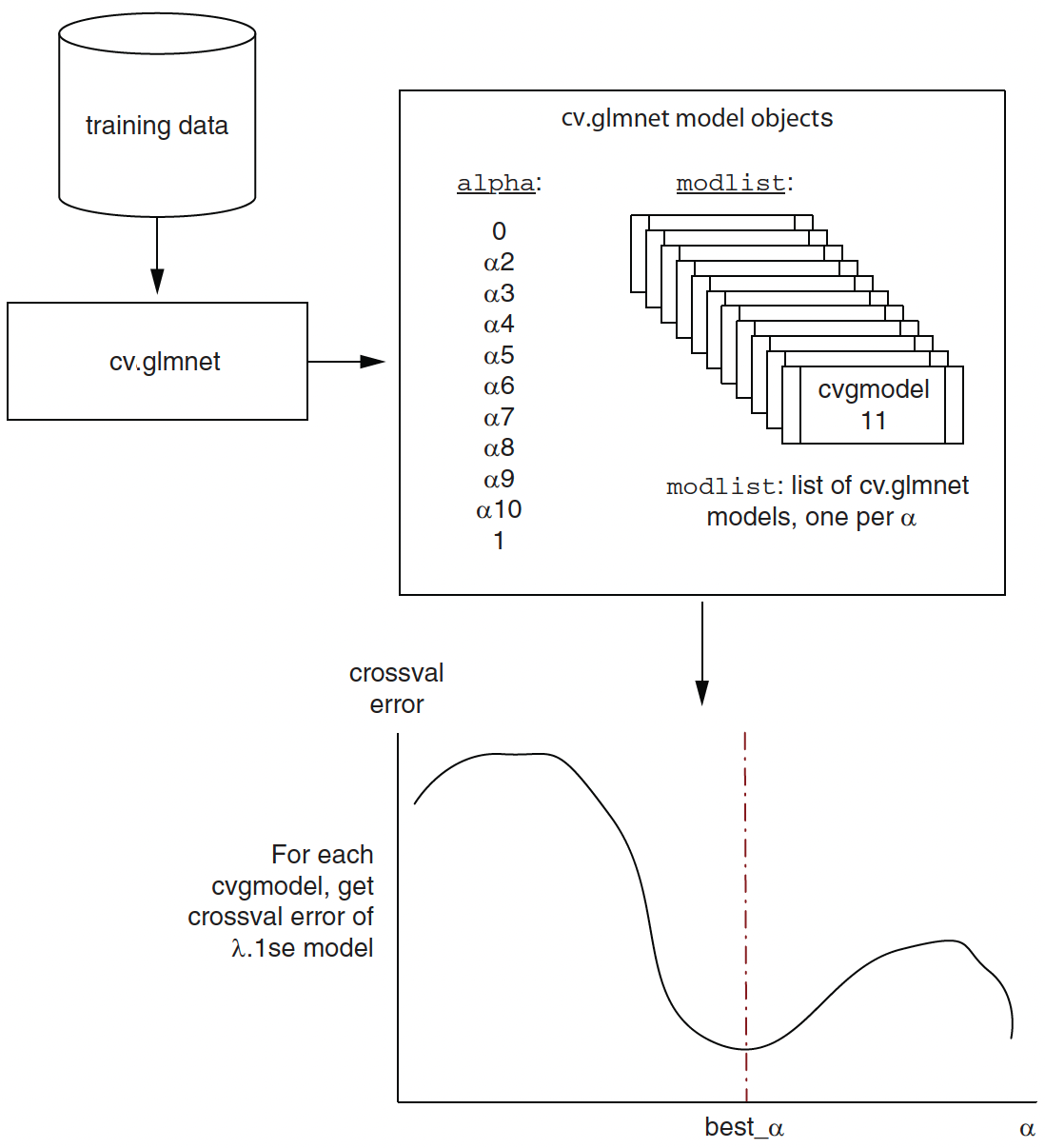

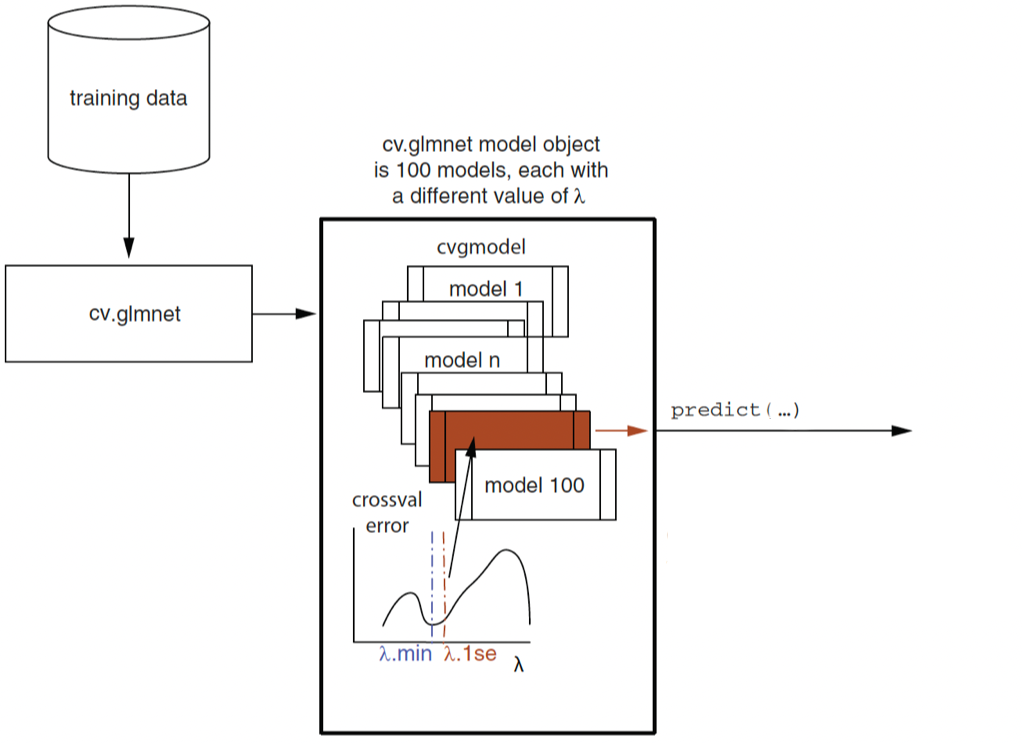

Lasso/Ridge Regression with Cross-Validation in R

- \(\lambda_{min}\): the \(\lambda\) for the model with the minimum cross-validation (CV) error

- \(\lambda\texttt{.1se}\): corresponds to the model with cross-validation error, which is \(\textit{one standard error (se)}\) of CV error above the minimum CV error.

Elastic Net Regression with Cross-Validation in R